The memoirs, adventures and ramblings of a superannuated precious metals trader.

“Silver never fails to disappoint”

I’ve been saying this since 1980. Does that mean silver is not a worthwhile investment?

Major cycles have turned, silver sentiment has turned positive, but keep expectations realistic.

When I entered the bullion market in mid-1980, silver was priced at $16 per ounce. Earlier that year, it had started at $40 per ounce, soared to $50 per ounce, and then crashed to $10 per ounce on ‘Silver Thursday’ (March 27, 1980) before recovering to the high teens. This turmoil was triggered by the Hunt brothers, who attempted a market squeeze by buying up silver futures and taking delivery, along with acquiring any other available silver stocks. The U.S. government intervened by implementing caps on the size of derivative futures positions on the exchanges and raising margin requirements retrospectively, effectively ending the Hunt brothers’ campaign. This led to a significant decline in interest in silver and other commodities until the late 1990s and is why many US Investors hold their precious metals offshore, in safe havens such as Singapore.

By the early 1990s, silver was trading below $5 per ounce—at or even below the cost of production. By the mid-1990s, silver was stuck in a narrow range around $5 per ounce, with very little interest and low trading volumes.

Before I left a well-established bullion bank in 1997 to trade for Mr. Marc Rich—both at his trading company and his personal investment office, I was the fifth reserve silver trader (out of only six traders). This meant I only got the short straw of making a two-way market in silver two or three times a year. This was fortunate; silver traded in lots of 100,000 ounces (referred to as 1 lac, from the Indian term for 100,000) with a narrow 2-cent spread, but it rarely moved more than 1 cent per ounce in a day. The challenge was that if someone traded at your quoted price, you needed to adjust your next price to cover your previous position to hopefully attract another trade to cover your exposure, otherwise you must accept someone else’s price to exit the position. The best you could hope for was to break even by the end of the day. The bank’s policy was strict: no more than a 300,000-ounce position during the day and absolutely no open positions overnight.

In the autumn of 1997, after joining Marc Rich Investments, I noticed that silver borrowing rates were becoming expensive while gold was declining from $325/oz to below $300/oz. When silver

hit $5.00/oz, I held a long position of 300,000 ounces. Mr. Rich asked me about my silver position, and I nervously answered. Instead of exploding as I expected, he calmly asked why. I explained the market tightness (seen in the raised borrowing costs for silver) and the move above $5.00. He got rather cross, not because of the position itself, but because he believed I should have been long a million ounces if I was that confident.

The next day, silver moved up by 8 cents (compared to the usual 1 cent), and Mr. Rich congratulated me on predicting the move. He then asked about my current position, and I proudly told him I was now holding one million ounces. He became angry again, saying that was the position I should have held the day before, and I should now be holding two million ounces if I truly believed in my assessment.

For several weeks, we aggressively built our position, sometimes buying over two million ounces in the morning and locking in profits by selling back one million ounces at a higher price later in the day. By early 1998, we had accumulated tens of millions of ounces of silver, while lending out only a small portion of the position to the market at over 10% per annum.

However (there’s always a “however”), our activity started drawing attention, especially from colleagues trading copper. They convinced Mr. Rich that with copper prices collapsing, silver would likely follow. We liquidated half of our silver position in a single morning. Ultimately, we had bought silver at an average price of just over $5.00/oz and sold it at just under $7.00/oz, making more than 180 cents/oz (a 36% gain in three months) on tens of millions of ounces.

The following month, silver continued to rise by nearly another dollar per ounce above our sell point, but it returned to $5.00/oz within six months. What’s the lesson here (other than me being a smart arse)? You don’t need to buy at the lowest point or sell at the highest to make a solid return. Recognise when a trend is breaking and then buy in, several old market sayings articulate “Do not try and catch a falling anvil”, or as more popular one goes, ‘He who trys to pick bottoms gets smelly fingers.’

More importantly, ‘The trend is your friend’—stick with the market momentum. It’s essential to see the bigger picture.

A crucial takeaway in the pricing mechanism is that despite enormous silver stocks (with London vaults overflowing to the point that any UK vault was accepted as loco London), borrowing costs for silver were still spiking higher. This happened because large holders like us were lending only a

small fraction back to the market. Those short on physical silver, even if they held long futures or forward contracts, had to either pay over 10% interest or buy silver for immediate delivery.

Fast forward to Year 2020…

We saw another big spike in the silver price in mid 2020 as several influential internet sites called on investors and the great unwashed (the general public at large) to buy silver because the big investment banks were hugely short silver futures, keeping the price depressed at $15/oz, when it should be $500/oz. By buying physical silver it would force the price higher and bankrupt all those evil investment banks. While initially in the first few days this did hurt the banks as big margin calls landed on their huge short futures positions, ultimately they made a fortune, as what the internet failed to recognise, was that while they were short the futures, they were long the physical, so simply delivered silver bars from their vaults against the futures contracts, silver for physical delivery having moved to a huge premium.

As usual, the investment banks came out hundreds of millions of dollars ahead. I’m not one for conspiracy theories, but, I could almost believe that one of the investment banks scattered a group of interns around New York’s internet cafes telling people to buy silver, not because it was a good investment, but that it would hurt the evil investment banks. If true, the investment banks really are evil (that I can believe).

So why invest in silver if it’s a series of short-term spike opportunities?

First, let’s dispel another myth: the Gold/Silver ratio. This concept is outdated and has been largely irrelevant since the early 18th century, when Sir Isaac Newton initiated efforts to balance the value of silver and gold.

As Master of the Royal Mint from 1699 to 1727, Newton was responsible for overseeing Britain’s coinage system. In this role, he evaluated the relative market values of gold and silver and, in 1717, established the official mint prices of gold and silver per ounce. This created a fixed gold-silver exchange ratio of 15.2 to 1.

This ratio closely matched the prevailing market rate at the time, stabilizing the relative values of gold and silver coins in circulation. As a result, it became easier for the public to accept gold as the primary monetary standard.

The bullion value of silver outside Great Britain, moved higher than the face value of the coin (something that still exists with “bullion” coins), causing silver to flow out and gold to flow in. By the early 19th century Great Britain’s reserves were entirely in gold, despite technically still being on a bimetal system. Other nations followed suit, so that by the late 19th century, most of the major powers were on the “Gold Standard” even if some were still in name bimetal. Gold remains a de-facto ‘reserve currency’. Silver is not. Therefore, comparing silver to gold is like comparing coal to oil or horses to cars.

So, let’s look at silver in it’s own right. Again, at very first glance, it’s not great news. While there is an increasing industrial demand for silver, the faster increase in demand for other metals such as copper, means an even larger increase in silver produced as a by-product of base metals, add to that ETF sales are adding more silver back into the supply chain.

But the world is presently experiencing a global supply-demand deficit in yearly production versus demands, and silver industrial demand is rising fast.

There is much good research on silver and well-reasoned commentaries on the fundamentals and economics of silver, or the debasing effects of the global debt crisis and deteriorating macro- economics on why silver is a good investment right now, but we must also look at the psychology surrounding silver.

What has changed? Sentiment. Ultimately, the market is always right; regardless of what the macro-economics, micro-economics, fundamentals, technical charts and what the bloke in the pub says. The price is the price. Take it or leave it. Now is the time to take it.

Silver typically recovers first and most rapidly following a financial crisis. Its low correlation with other metals and assets makes it a valuable addition to a diversified investment portfolio.

Does it matter that Government legislation to de-carbonise, will increase demand for silver? Yes.

Does it matter that London vault stocks stand at 26,618 tonnes (LBMA vault data) and New York silver stock for Comex stand at 9,436 tonnes, totalling over 36,000 tonnes (approximately 18 months of production) tonnes of silver? No.

As we have seen in 1971-1980 and 1997-1998, or 2003-2011 or year 2020, there is a difference between stock held and stock available for market liquidity (my trading example earlier).

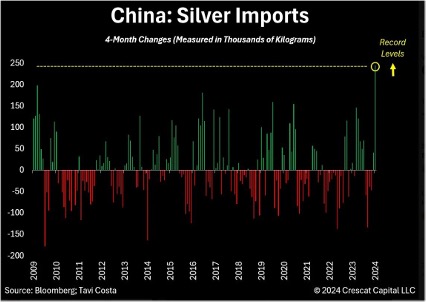

Much of the stock declared is already allocated to contracts, margin and as security. Currently silver is at full carry. IE the interest on silver is zero, but it only takes a small buying spree; just some metal swaps not to be rolled over; or more likely, an increase in physical demand (physical demand in India alone is running at over two thousand tonnes a month and steadily increasing as lower taxes cut in), while China is making record Silver imports while at the same time is a leading global silver producer.

What are the similarities here ?…. Major global systemic crises have consistently been proven to trigger significant price rallies in silver. Is this driven by its role as a store of wealth or as a protective hedge?

Silver rallied hard into all these events….

- Stagflation Crisis : 1973 Oil Crisis, impacting significant Stagflationary repercussions that rolled into the 1980s Latin American Debt Crisis

- 1997-98 Asian Financial Crisis:

- Commodity boom leading directly into 2007-2008 Global Financial Crisis: and ultimately into 2010 European Sovereign Debt Crisis

- 2020 COVID-19 Pandemic Crisis:

Black swans are presently everywhere to be seen, suddenly we’re back to the price squeezes of the late 70’s into 1980, 1997 into1998, 2008 into 2011, and year 2020 etc. The fact that the macro- economics, the micro-economics, the fundamentals, the charts and the bloke in the pub all say that silver is due to continue and even accelerate this trend only adds more weight to the whole picture. Interestingly, silver starts to make it’s upward moves in late August or early September.

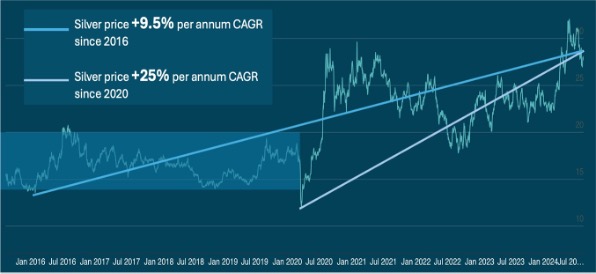

But here’s the real story. Silver, despite it’s short-term volatility, is on a well-defined upward trend that compares well with most other assets and investments. Depending on where you want to pick your peaks and troughs. Silver is set to return conservatively 12-15% per annum for the current long-term trend; some could rightly claim 30% per annum mid-term. Not bad if you consider that 8% per annum will see the price double in ten years. It makes sense for silver holdings to be a good component of an investment portfolio.

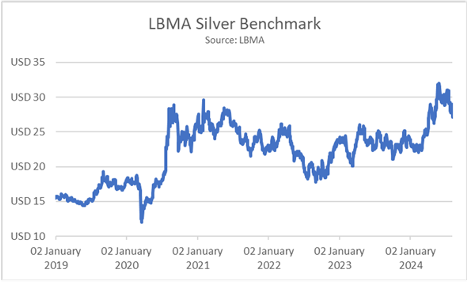

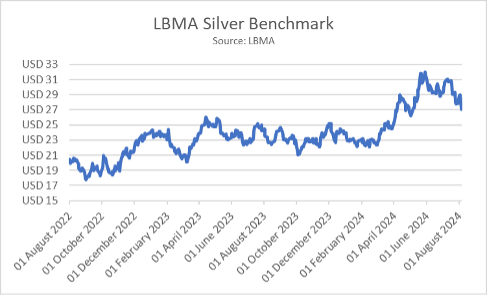

Chart above I would strongly suggest the new silver bull cycle did not start until January 2020.

Will you be disappointed by silver? Well that depends on your expectations. If you’re expecting an immediate short-term return of 1,000%, then I would suggest you go to Happy Valley, Goodwood or Newmarket and enjoy yourself; you might get lucky. Invest in silver and you have almost unlimited upside and very little downside in this cycle. What we traders call the risk/reward ratio.

If you want something in your portfolio that is likely to give you a better return than more traditional, but now very tired assets (end of the economic cycle), silver won’t disappoint.